The Sniper’s Tax

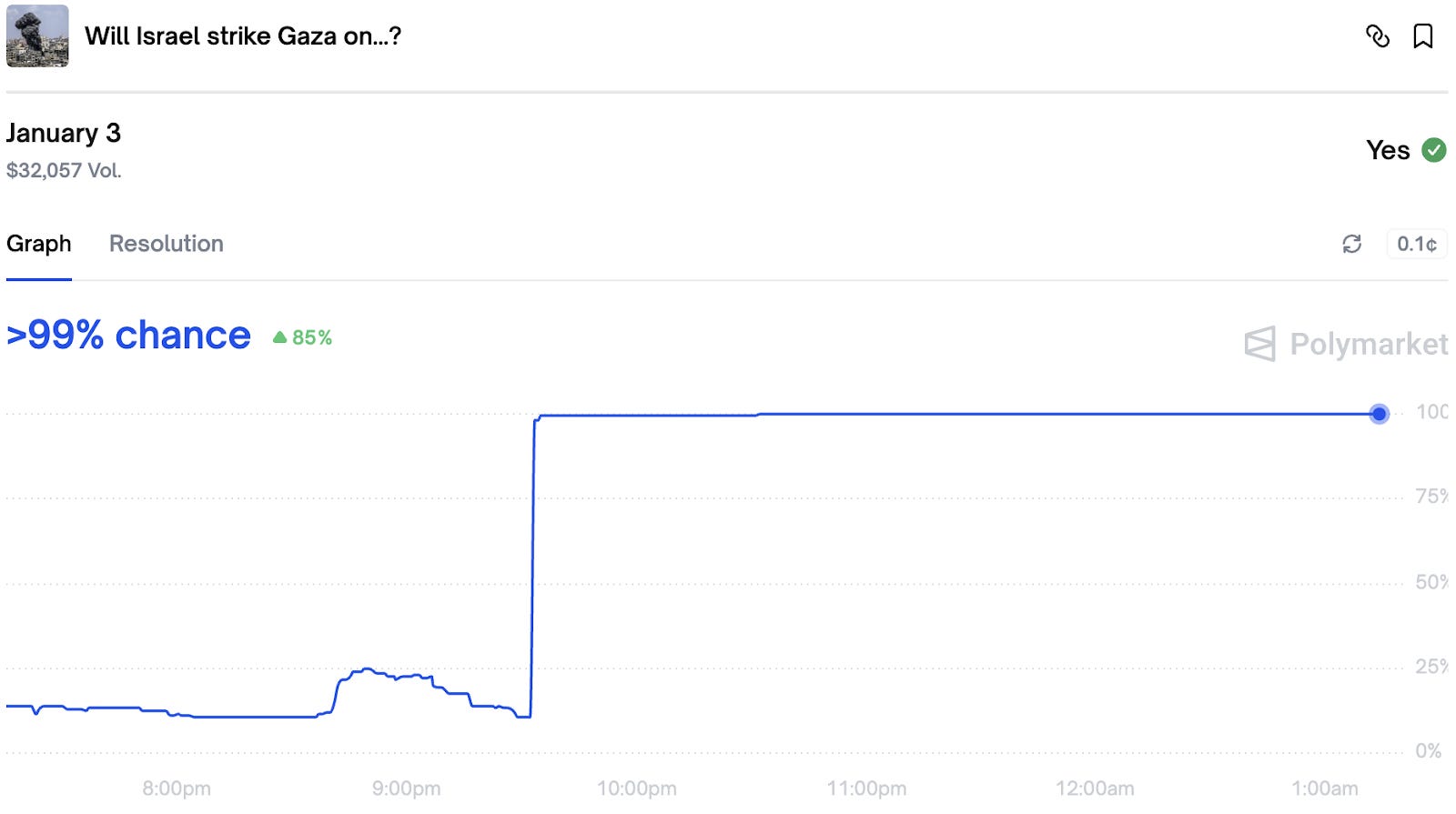

On January 3, 2026, a trader named "dudukos" cleared the entire order book of the "Will Israel strike Gaza on January 3, 2026?" market in a single trade, buying from $0.10 all the way up to $0.80. He did this again on January 10, 11, and 12. Same pattern on dozens of other Israel strike markets.

This wasn't brilliant geopolitical analysis. Dudukos didn't know something the market makers didn't know. He just found out slightly faster — fast enough to buy their resting orders before they could cancel them. The market makers posted offers at 10 cents because they thought the probability of a strike was around 10%. Then a strike happened, the probability went to ~100%, and dudukos bought all their 10-cent offers before they could pull them. A good day for dudukos. A bad day for liquidity providers.

Polymarket and Kalshi solved the hard v1 problems: getting users, staying legal, and building trust. Existential stuff. But the market structure was inherited from traditional finance without much questioning of whether it fits. Traditional stock exchanges use continuous limit order books, and so does Polymarket.

The problem is that prediction market assets are binary and news-sensitive in a way that stocks aren’t. Apple might gap down 3% on bad earnings. A “will there be a strike today” contract goes from 10 cents to 99 cents in the time it takes to read a tweet. In traditional markets, being slightly slower than the fastest trader costs you a few basis points. In prediction markets, it costs you the entire value of your position. This is bad for market makers.

There is a known fix for this problem. It’s called a batch auction.

Who's in the market

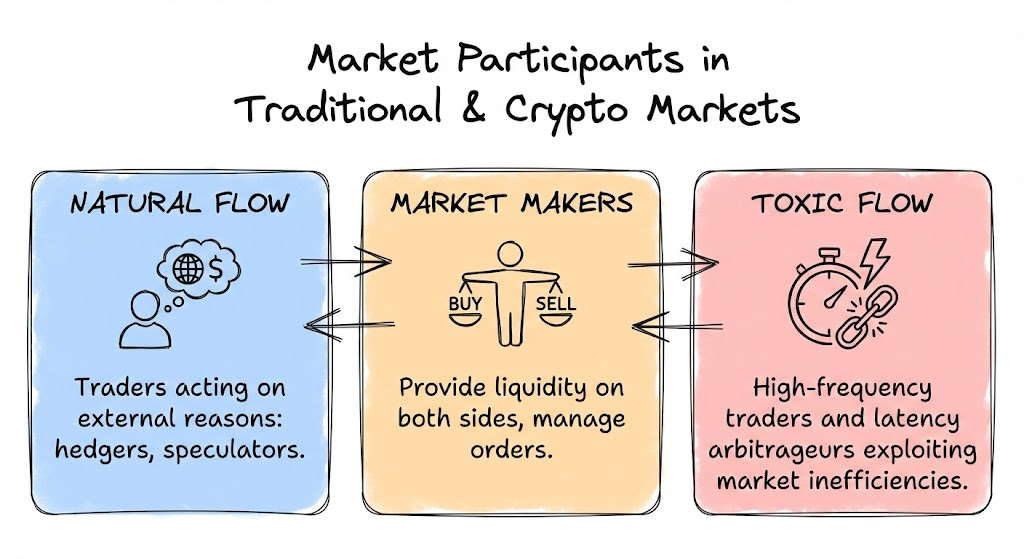

Any market has three kinds of participants:

Natural flow. People who actually want to trade — hedgers, speculators, someone with a thesis. In prediction markets, this includes professional forecasters, gamblers, and the occasional person who genuinely wants to hedge against a Trump presidency or whatever.

Market makers (MMs). They post bids and offers so that when you want to buy, there’s someone to buy from. They make money on the spread, and they lose money when they’re wrong about the price. The job is basically: be a liquidity vending machine, try not to get run over.

Toxic flow. People trying to run over the market makers. High-frequency traders, latency arbs, anyone whose edge is “I react to information faster than you can update your quotes”. This flow is toxic to market makers in the first order, but also to the market as a whole in the second and third – through degraded outcomes for non-toxic flow.

The dynamic plays out predictably. Toxic flow eats market makers. Market makers respond by widening spreads and posting less size. Trading gets worse for everyone. The market makers who survive are the ones who spend enough on speed to avoid getting picked off, which raises the cost of market-making, which raises spreads, which means you pay more to trade.

Traditional exchanges have developed various band-aids: last look, trade rejections, payment for order flow, and tiered fee structures. These help, sort of. None of them fix the underlying problem.

The Prediction Market Twist

Prediction markets have the same participants, but the assets behave differently:

Natural flow is mostly forecasters and gamblers.

Market makers are still market makers. But the thing they’re making markets on can go from 10 cents to 95 cents in the time it takes to read a headline.

Toxic flow in prediction markets is murkier. The sniper who sweeps the book when a strike happens is bringing information into the market. The price discovery is real. In some sense, this is the whole point — we want markets to incorporate news fast.

The ultimate challenge lies in finding an equilibrium where the information gains provided by snipers don’t come at the cost of bankrupting the market makers who provide the necessary liquidity.

The unhedgeable problem

If you’re a market maker holding too much Apple, you can sell Nasdaq futures. Imperfect, but it works. If you’re a market maker holding too much “Will Israel strike Lebanon today?” — what do you hedge with? There’s no correlated instrument. You’re just... exposed.

Example: Imagine you are an MM providing liquidity for “Will Israel strike Lebanon today?” with a spread around $0.20. Suddenly, news of a strike breaks on X.

On the offer side: someone buys your YES tokens at 22 cents. Fair value is now 99 cents. You sold a dollar for 22 cents.

On the bid side: someone sells you NO tokens at 78 cents. Fair value is now 1 cent. You paid 78 cents for trash.

Either way, you lose. Not because you were wrong about the probability — you might have been perfectly calibrated five minutes ago — but because your cancel button was slower than their react button. You weren’t providing liquidity to a forecaster. You were exit liquidity for a bot.

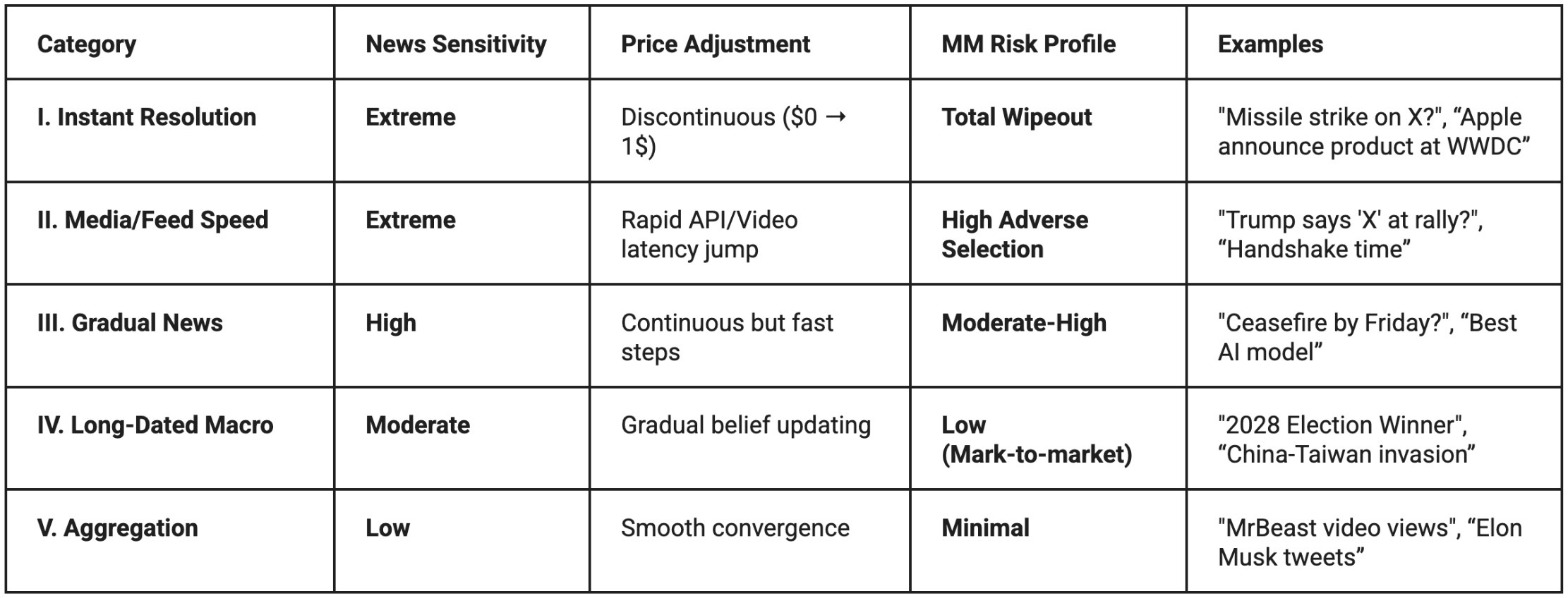

Not all markets have this problem equally. The risk depends on how "jumpy" the news is.

From this table, a clear pattern emerges: the markets with the highest social value and information content – those with extreme or high news sensitivity – are precisely the markets in which passive liquidity is most difficult to sustain.

The math

A market maker's expected profit (E[π]) looks roughly like this:

Where s is the spread, V(s) is volume (which drops as the spread widens), Pnews is the probability of a jump event, and, Lsnipe is the loss when a sniper picks off your stale quote.

In traditional markets, Lsnipe is a few ticks. Annoying, survivable. In prediction markets, it can be 80 cents on the dollar. When Pnews is high — any geopolitical market, any breaking-news market — the sniping term dominates.

The MM has two ways to keep expected profit positive: widen s, or pull quotes entirely. Both make the market worse for everyone else. This isn't a failure of will. It's the only rational response. (The Daedalus Research Team's "Toward Black-Scholes for Prediction Markets" walks through the full framework).

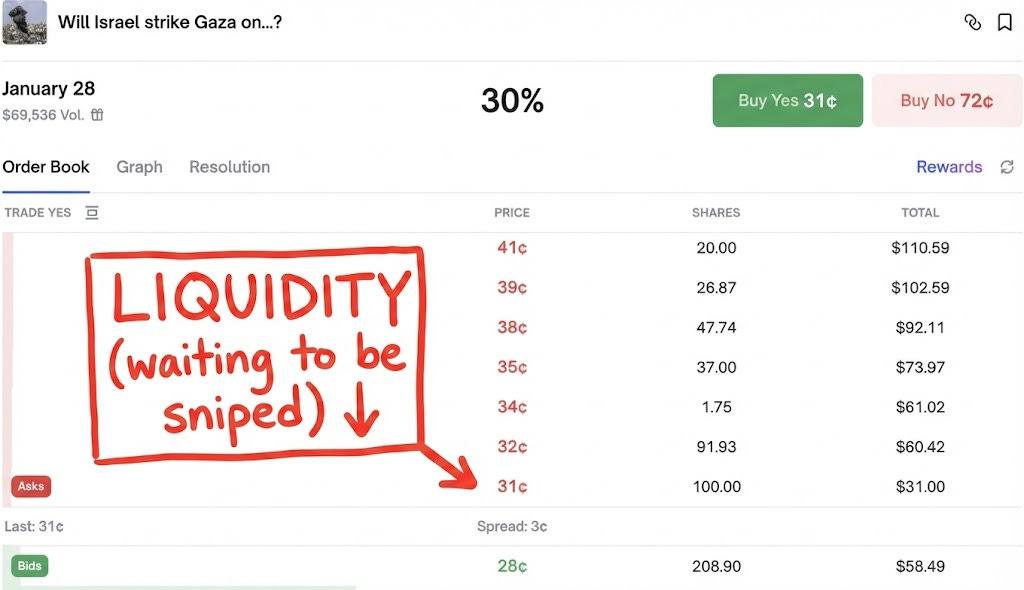

This creates the "liquidity mirage" problem. At 3am on a quiet Tuesday, you can see a reasonable order book. But that liquidity isn't really there — it'll vanish the instant there's actual news to trade on. And once the real liquidity is gone, the market becomes trivially manipulable. You can shove the price around with a few thousand (often - hundreds) dollars.

Who's left holding the bag

So if professional market makers won’t provide liquidity on the scary markets, who does?

Polymarket and Kalshi burn millions of dollars a year on liquidity incentive programs — basically paying people to post orders. The pitch is: earn rewards for providing liquidity. The reality is: you’re being paid to stand in front of the train.

Retail LPs don’t have millisecond infrastructure. They don’t have hedging desks. They’re posting orders from a browser tab while the news breaks on X and someone’s bot reacts in 400ms. The incentive programs technically compensate for this, except they don’t — the rewards have shrunk as the platforms scaled, and they were never designed to cover “you just lost 80 cents on every contract you quoted”.

The result is a quiet subsidy flowing from retail liquidity providers to sophisticated snipers. The retail user thinks they’re earning yield. They’re actually exit liquidity, again.

The fix

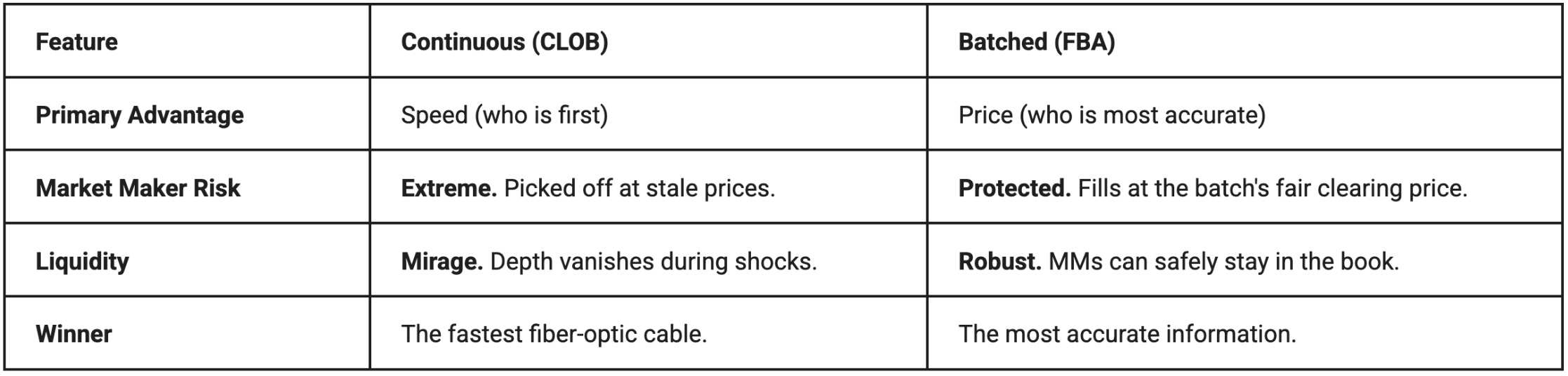

The problem isn’t that we need faster infrastructure. The problem is that continuous-time markets reward speed over accuracy. This is a known result — Budish, Cramton, and Shim showed it formally in 2015. Even in traditional equities, continuous limit order books systematically favor the fast over the informed. In prediction markets, where prices can move 80 points in a tick, it’s worse.

The solution is to stop trading in continuous time. Instead: frequent batch auctions (FBAs).

How It Works

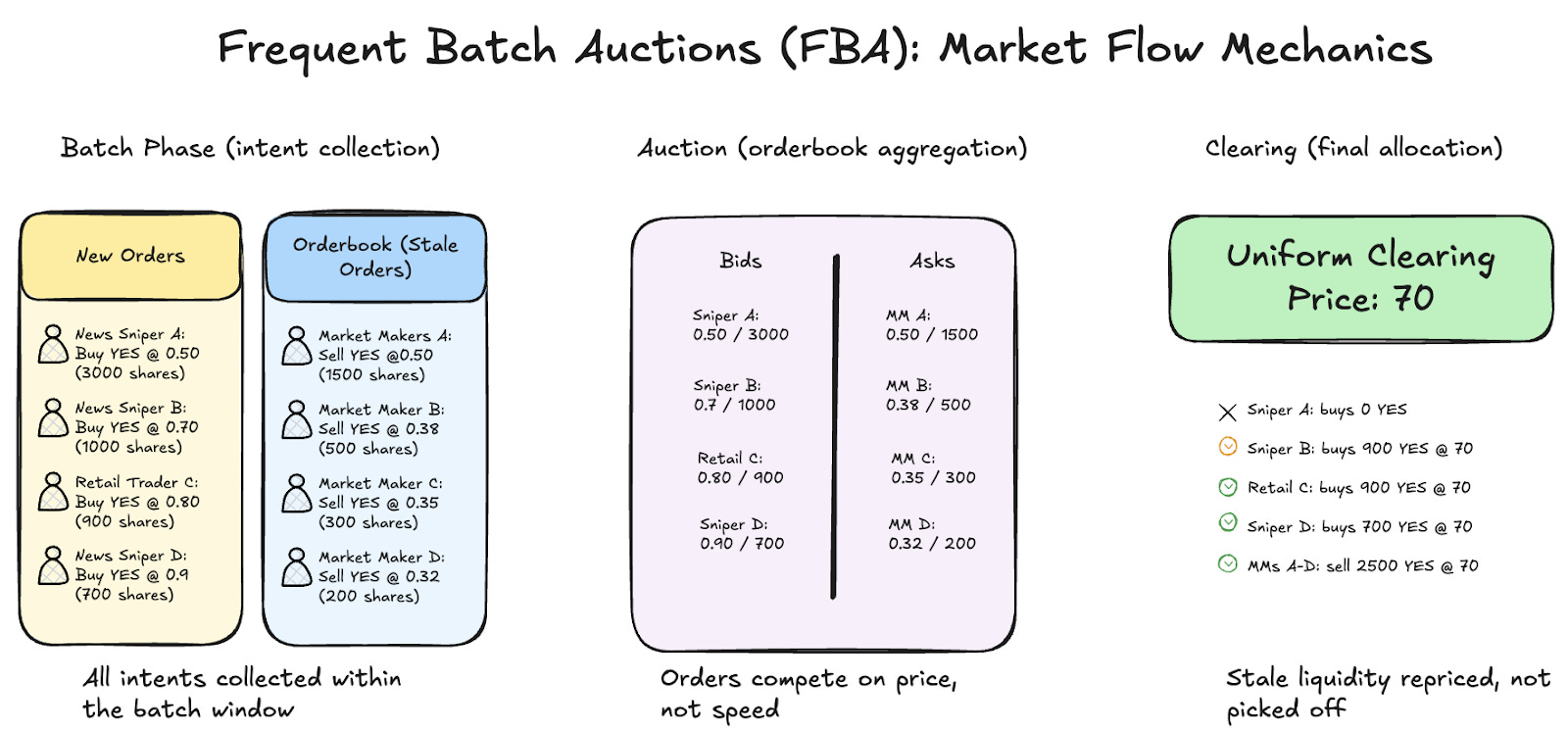

In a continuous order book, if news breaks at 12:01:00.001, the sniper who hits the order at 12:01:00.002 wins. First come, first served.

In a batch auction, the market runs on a heartbeat — say, every 30 seconds. All orders submitted during that window get collected, then the exchange computes a single clearing price that maximizes overall welfare. Everyone in the batch trades at the same price.

The mechanics:

Collect. Orders accumulate during the batch window — buys, sells, cancellations, everything.

Match. Instead of executing in arrival order, the exchange aggregates supply and demand.

Clear. One uniform price for the whole batch. If you’re buying and I’m selling and we overlap, we trade at the clearing price, not at whatever stale quote happened to be sitting there.

Speed vs. price

This changes what traders compete on.

In a continuous book, the competition is: who reacts first. Trader A and Trader B both see the news. Trader A’s bot fires 50ms faster. Trader A wins, Trader B gets nothing. The margin of victory is latency.

In a batch auction, Trader A and Trader B both land in the same batch. Now the question is: who’s willing to pay more? If A bids 80 cents and B bids 85 cents, the clearing price moves toward 85. The winner is whoever valued the contract higher, not whoever had the shorter wire to the exchange.

The money that used to go to “I was 50ms faster” now goes to “I was right about the price”. That’s just better. The same information gets into the market, but the rents flow differently — toward accuracy instead of infrastructure.

Why this helps market makers

Here’s the key insight: in a batch auction, stale quotes don’t get picked off at stale prices.

Say you’re a market maker with an ask sitting at 20 cents. News breaks. In a continuous book, a sniper buys your 20-cent ask before you can cancel it. You sold a dollar for 20 cents. Done.

In a batch auction, your 20-cent ask is still there when the batch runs — but it doesn’t fill at 20 cents. The batch aggregates all the new buy orders from people who saw the news, the clearing price comes out at 75 cents, and your shares sell at 75 cents. You got the fair price, not the stale price.

This is a big deal. Market makers currently price in a “sniping tax” on every quote — wider spreads, less depth, quotes pulled during volatile periods. If that tax goes away, they can quote tighter and deeper. Budish’s research on equity markets bears this out: batch auctions don’t just “slow things down,” they actually tighten spreads.

This shifts the competitive frontier from network hardware to predictive intelligence. You stop rewarding the fastest connection and start rewarding the best information.

So what

Polymarket and Kalshi proved the demand is real. People want to trade on real-world events. The volume is there, the user interest is there, the legal questions are mostly settled.

But the market structure is wrong. Continuous order books work fine when prices move smoothly. Prediction markets aren’t smooth — they’re binary events where the price can jump 80 points in a tick. Importing the CLOB model from traditional finance made sense as a starting point, but it’s a bad fit for the asset class. The result is a system that bleeds liquidity providers and rewards infrastructure over insight.

Batch auctions fix the core problem. Not by slowing things down, but by changing what traders compete on. Speed stops mattering. Price starts mattering. Market makers can actually do their job without getting run over every time news breaks.

This isn’t a minor optimization. It’s the difference between prediction markets that sort of work and prediction markets that actually work.

We should probably build the second kind.